The Real Cost of Buying Property in Malaysia as a Foreigner: 8% Stamp Duty Explained (2026)

Something changed on 1 January 2026 that most foreign buyers have not properly priced in. The Memorandum of Transfer (MOT) stamp duty for non-citizens on residential property doubled — from 4% flat to 8% flat. On a RM 1.5 million condo, that is RM 76,000 more than a Malaysian citizen pays for the same transfer. This guide breaks down every cost layer, how it compares globally, and the one structural option that meaningfully reduces the burden.

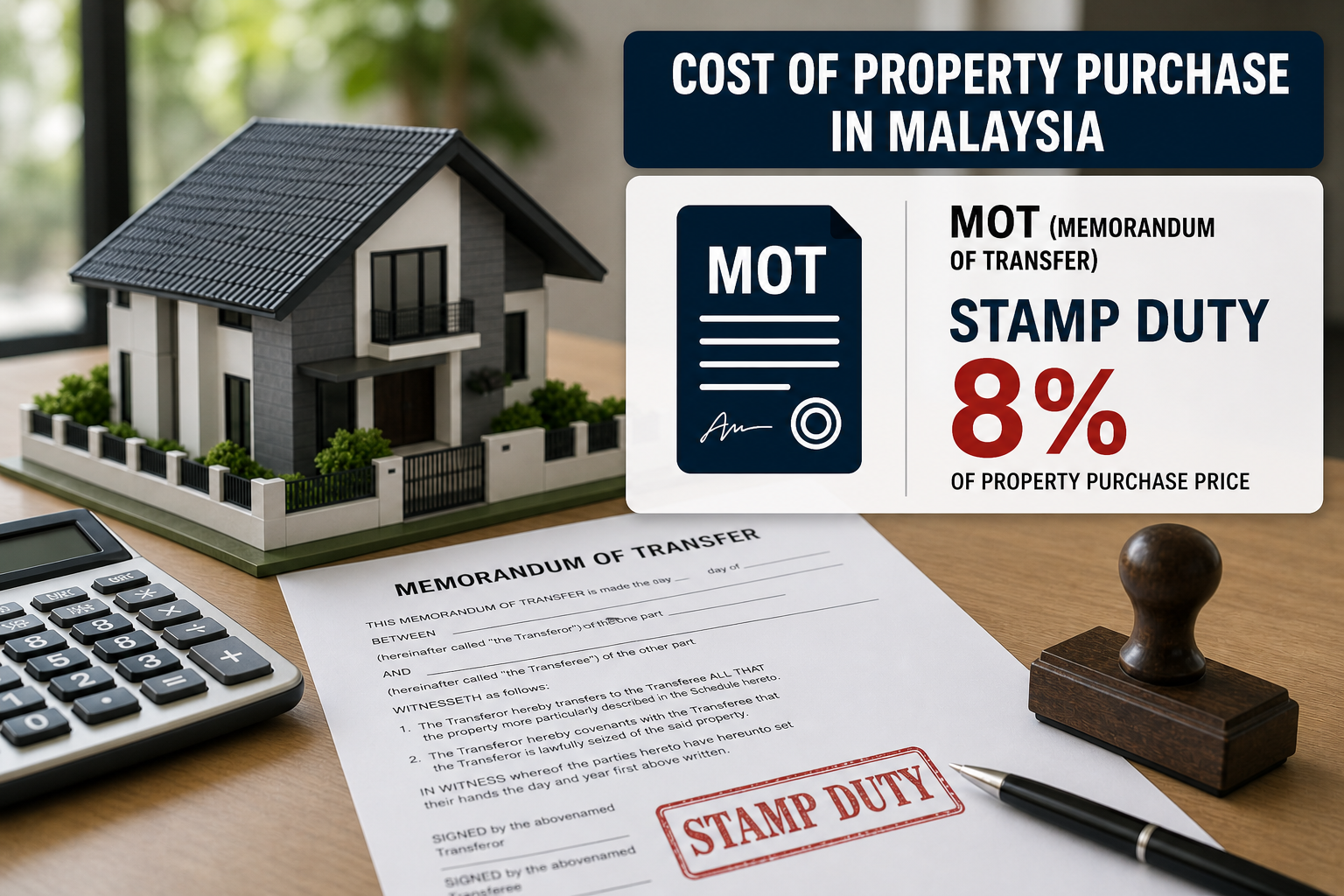

What Changed in 2026

Under the Malaysian government's Budget 2026, the MOT stamp duty rate for non-citizens purchasing residential property was raised to a flat 8%, effective from 1 January 2026. This replaced the flat 4% rate that had been in place since 2024, and the earlier tiered-for-all regime before that.

The MOT — Memorandum of Transfer — is the legal document that records the transfer of property title from seller to buyer, and it is registered with the land office. The stamp duty paid on the MOT is a government tax triggered at the point of transfer, typically upon handover of a completed property or upon registration of a subsale transaction.

For Malaysian citizens, the rate structure did not change. They continue to pay tiered rates of 1% to 4%, applied in tranches. For foreign nationals and foreign-owned companies, the new flat 8% rate applies to the full purchase price of any residential property — no tiers, no tranches.

This applies to residential property only. Commercial, industrial, and mixed-use commercial strata (such as office suites and shop lots) are not subject to the 8% rate. The surcharge is specifically targeted at residential dwellings: condominiums, apartments, service residences, SOHOs, and landed houses.

Citizens vs Foreigners: The Rate Gap

The divergence between citizen and foreigner stamp duty is now the starkest it has ever been. For context:

| Buyer Category | MOT Stamp Duty Structure | On RM 1.5M Property |

|---|---|---|

| Malaysian citizen / PR | 1% (first RM 100K) → 2% (next RM 400K) → 3% (next RM 500K) → 4% (above RM 1M) | RM 44,000 |

| Non-citizen / foreign company | Flat 8% on full purchase price | RM 120,000 |

| Difference | — | RM 76,000 more as a foreigner |

The calculation for foreigners is straightforward: multiply the purchase price by 0.08. There are no thresholds, no exemptions, and no reliefs available to reduce this figure. The citizen formula is more nuanced, but as a quick reference, on any property above RM 1 million: citizen stamp duty equals RM 24,000 plus 4% of the amount above RM 1 million.

Worked Examples at Key Price Points

Since foreigners are required to purchase above state minimum thresholds — RM 1 million for most residential property in Kuala Lumpur and Selangor — the relevant range starts at RM 1 million and goes up. Here is how the numbers play out:

| Purchase Price (RM) | Foreigner MOT (8% flat) | Citizen MOT (tiered) | Cost Gap (RM) |

|---|---|---|---|

| 1,000,000 | 80,000 | 24,000 | 56,000 |

| 1,500,000 | 120,000 | 44,000 | 76,000 |

| 2,000,000 | 160,000 | 64,000 | 96,000 |

| 3,000,000 | 240,000 | 104,000 | 136,000 |

| 5,000,000 | 400,000 | 184,000 | 216,000 |

The gap widens in absolute terms as the property price increases, though the proportional difference remains roughly constant. At RM 1 million, foreigners pay more than three times the citizen rate. At RM 5 million, it is still over twice as much.

Additional Costs Foreigners Pay That Citizens Do Not

The 8% stamp duty is the largest foreigner-specific cost, but it is not the only one. Three further charges apply exclusively — or disproportionately — to foreign buyers:

State Consent Fee

Every residential property purchase by a non-citizen requires approval from the relevant State Authority under Section 433B of the National Land Code. The consent process is not optional and cannot be waived. A fee is payable upon application, the amount of which varies by state:

| State | Consent Fee (Approximate) |

|---|---|

| Kuala Lumpur (Federal Territory) | RM 10,000 – RM 20,000 |

| Selangor | RM 10,000 – RM 20,000 |

| Johor | RM 10,000 – RM 20,000 |

| Penang | RM 10,000 + ~1% additional levy on purchase price |

| Other states | RM 5,000 – RM 20,000 |

Penang's additional 1% state levy on foreign purchases is particularly significant — on a RM 1.5 million property, it adds RM 15,000 on top of the consent fee itself. Malaysian citizens pay neither of these charges.

No Access to Stamp Duty Exemptions

Malaysian citizens buying their first home priced below RM 500,000 are eligible for a full stamp duty exemption on both the MOT and loan agreement — an exemption extended by Budget 2026 through to 31 December 2027. Foreigners cannot access this exemption under any circumstances. In practice this matters less for most foreign buyers since the RM 1 million minimum purchase threshold in KL already exceeds the exemption ceiling, but for markets with lower thresholds such as Sabah and Sarawak, the exclusion is meaningful.

Higher Down Payment Requirement

Malaysian banks typically advance 50–70% loan-to-value (LTV) to foreign buyers, versus 80–90% for citizens. On the same RM 1.5 million property, a citizen with 90% financing puts down RM 150,000. A foreign buyer at 60% LTV must produce RM 600,000 upfront. That RM 450,000 difference is cash locked out of any other use — its opportunity cost is real, even if not itemised on any closing statement.

Total Acquisition Cost: A Complete Side-by-Side

Putting every cost layer together for a RM 1.5 million condominium purchase in Kuala Lumpur:

| Cost Item | Malaysian Citizen | Foreign Buyer (2026) |

|---|---|---|

| MOT stamp duty | RM 44,000 | RM 120,000 |

| Loan stamp duty (0.5% of loan) | RM 6,750 (at 90% LTV) | RM 4,500 (at 60% LTV) |

| SPA legal fees (approx.) | RM 15,000 | RM 15,000 |

| Loan agreement legal fees (approx.) | RM 12,000 | RM 12,000 |

| Valuation fee | RM 3,500 | RM 3,500 |

| State consent fee | RM 0 | RM 10,000 – RM 20,000 |

| Total transaction costs | ~RM 81,000 (~5.4%) | ~RM 165,000 – RM 175,000 (~11–12%) |

| Down payment required | RM 150,000 (10%) | RM 600,000 (40%) |

| Total cash needed at closing | ~RM 231,000 | ~RM 765,000 – RM 775,000 |

The total upfront cash gap between a citizen and a foreigner buying the same RM 1.5 million property is over RM 500,000. This is the true cost of foreign property ownership in Malaysia at this price point — not just the headline stamp duty number.

How Malaysia Compares Globally

Context matters. Despite the sharp increase, Malaysia's 8% flat stamp duty for foreigners remains significantly lower than the effective surcharges applied in neighbouring markets:

| Country | Foreign Buyer Transfer Tax / Stamp Duty |

|---|---|

| Singapore | 6% buyer stamp duty (tiered) + 60% Additional Buyer Stamp Duty (ABSD) |

| Hong Kong | Up to 4.25% Ad Valorem Duty + 15% Buyer Stamp Duty (non-PR) |

| Australia (Victoria / NSW) | Standard duty + ~8% foreign purchaser surcharge |

| Thailand | ~2% transfer fee; foreign ownership restricted to condos (max 49% of building) |

| Malaysia (from 2026) | Flat 8% MOT stamp duty on residential property |

Singapore's ABSD is effectively punitive — 60% on top of standard duty makes residential investment by foreigners almost structurally unviable. Hong Kong's 15% Buyer Stamp Duty plus restrictions is similarly deterrent-level. Malaysia at 8% remains competitive as a destination for foreign capital, even post-2026, relative to the immediate regional peers. Thailand is cheaper but restricts ownership structure; Australia applies similar surcharges to Malaysia's in key states.

The increase is real and should be budgeted for. But it does not fundamentally alter Malaysia's relative attractiveness for buyers coming from Singapore or Hong Kong, where the alternative stamp duty regimes are far more expensive.

Loan Stamp Duty: The One Cost That Favours Foreigners

There is a counterintuitive footnote in the cost comparison. Loan stamp duty — charged at 0.5% of the total financing amount — is the same rate for everyone. Because foreign buyers typically borrow less (lower LTV), they actually pay less in loan stamp duty than citizens financing the same property.

On an RM 1.5 million property, a citizen at 90% LTV borrows RM 1.35 million and pays RM 6,750 in loan stamp duty. A foreign buyer at 60% LTV borrows RM 900,000 and pays RM 4,500. The RM 2,250 saving is modest against the RM 76,000 stamp duty gap — but it is real. The foreign buyer's higher cash requirement is partly why the loan stamp duty bill is lower.

Exit Costs: RPGT Compounds the Picture

The 8% acquisition stamp duty is a sunk cost on entry. But foreigners also face a permanent capital gains tax on exit that Malaysian citizens do not, in the form of Real Property Gains Tax (RPGT).

| Holding Period | RPGT Rate — Foreigner | RPGT Rate — Malaysian Citizen |

|---|---|---|

| Years 1 – 5 | 30% on chargeable gain | 30% on chargeable gain |

| Year 6 onwards | 10% (permanent floor) | 0% (fully exempt) |

Malaysian citizens are fully exempt from RPGT after five years of ownership. Foreigners have no equivalent exemption — the 10% floor applies regardless of how long the property is held. Additionally, any buyer purchasing a property from a foreign seller is required to withhold 7% of the purchase price (versus 3% for citizen sellers) and remit it to LHDN as a provisional RPGT retention. If the actual liability is lower, a refund can be applied for; if higher, a top-up is due.

The full cost-of-ownership picture for a foreign buyer in Malaysia therefore layers across three levels: an 8% stamp duty on entry, a 30% flat tax on net rental income during the hold (for non-residents), and a minimum 10% capital gains tax on any profit realised at exit. Running each of these figures explicitly — rather than gross yield and asking price — is how experienced foreign investors evaluate Malaysian property.

The One Legitimate Way to Reduce the Impact

There is no legal mechanism to reduce a foreigner's MOT stamp duty rate — it is a statutory flat charge with no exemptions or reliefs available to non-citizens. Permanent residency is the only route to citizen-equivalent treatment, and that path is separate from property ownership itself.

What does exist — and it is genuinely uncommon — is developers absorbing the MOT stamp duty on behalf of the buyer as a promotional incentive on new launches.

In competitive new launch markets, particularly for high-rise residential developments targeting international buyers, developers occasionally offer a full stamp duty absorption package: the developer agrees to pay the 8% MOT stamp duty on the buyer's behalf as part of the purchase deal. Legal fees are often absorbed as a separate matter; the stamp duty absorption is the more significant concession.

The mechanics work as follows. The developer uses margin built into the project's pricing and sales budget to cover the stamp duty cost. The buyer still completes the purchase at the published price; the absorption is a developer contribution to the closing costs, not a price reduction. The legal effect is identical to paying the stamp duty directly — the transfer is registered with the same duties paid — but the cash does not leave the buyer's pocket.

On a RM 1.5 million unit, that is RM 120,000 the buyer does not need to produce. At the RM 2 million mark, it is RM 160,000. These are material numbers that shift the entry cost profile substantially — from a total acquisition outlay of roughly RM 165,000 in transaction costs down to approximately RM 45,000, which approaches citizen-equivalent territory.

Stamp duty absorption deals tend to appear in specific circumstances: new launches by developers with strong margins and an international marketing mandate, projects in KLCC, Mont Kiara, or Iskandar Puteri where the foreigner buyer is a primary target segment, and early-phase launches where the developer is incentivised to move initial units quickly to build presales momentum. They are not standard. They are not advertised the same way as price cuts. And they are not available on subsale or secondary market transactions — only on developer primary sales.

The rarity of these deals is precisely what makes them worth seeking out. Most foreign buyers price in the 8% and move on. Buyers who work with agents closely connected to developer sales teams — and who understand which launches are structured with foreigner cost absorption — arrive at the same asset with a materially lower cash requirement and a faster payback on the total investment.

If you are a foreign buyer evaluating Malaysian property in 2026, the 8% MOT stamp duty is not a reason to walk away from the market. But it is an 8% hurdle that every deal must clear before a single ringgit of yield or appreciation registers as genuine return. The most efficient path through that hurdle is to find projects where the developer has already priced it away.

Sources & References

- LHDN — Stamp Act 1949: First Schedule (MOT rates) and Item 22(1) (loan agreement rates)

- LHDN — Real Property Gains Tax: Schedule 5, RPGT Act 1976

- LHDN — Non-Resident Individual Income Tax Treatment (30% flat rate)

- Alestria Property — Malaysia Budget 2026: 8% Stamp Duty for Foreign Buyers

- Boon Giap — MOT Stamp Duty for Foreign Property Buyers in Malaysia 2025–2026

- Mah Weng Kwai & Associates — Section 433B National Land Code: State Consent Requirements

- PropCashflow — 8% Stamp Duty for Foreigners Malaysia 2026: What You'll Actually Pay