What's Actually Deductible on Your Rental Income in Malaysia

LHDN allows certain expenses to be set against your rental income — reducing the amount you're taxed on. But not everything you spend on a property qualifies. The line between an allowable deduction and a disallowed capital expense is finer than most landlords realise, and getting it wrong costs money in either direction.

The Tax Framework

Rental income in Malaysia is taxable under Section 4(d) of the Income Tax Act 1967. Unlike business income (Section 4(a)), rental income is treated as investment income — which means the range of deductible expenses is narrower. LHDN's general principle is straightforward: expenses are deductible if they are incurred wholly and exclusively in the production of that rental income. Expenses that are capital in nature — improving or enhancing the property rather than maintaining it — are not deductible under Section 4(d), regardless of how large or legitimate the expenditure is.

This single principle — revenue versus capital — determines whether any given expense qualifies. Everything else flows from it.

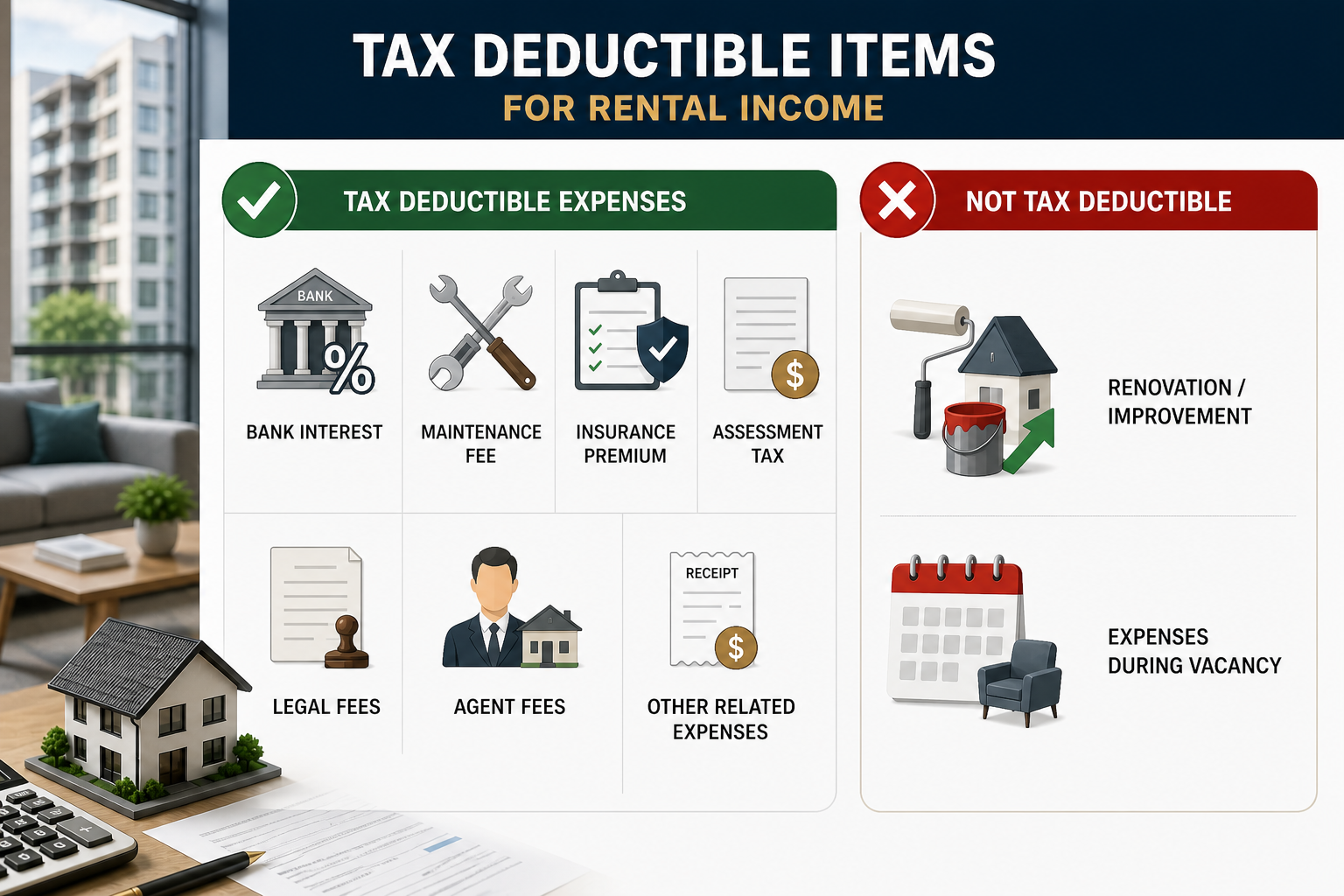

Bank Loan Interest

Interest on mortgage or property loan

If you are financing the property with a bank loan, the interest portion of your monthly repayment is deductible against rental income. The principal repayment is not — that is a capital transaction, reducing what you owe, not an expense incurred in producing income.

There is an important condition: the deduction only applies for periods when the property is tenanted and generating rental income. If the property is vacant, the interest incurred during that period does not qualify — LHDN ties the deduction to the production of income, not simply to the existence of the loan.

Your bank's annual statement or e-statement breaks down each monthly payment into interest and principal. Only the interest column is relevant. Keep these statements as supporting documentation for your tax return.

- Interest portion of monthly loan repayment — deductible while property is tenanted

- Principal repayment component — capital in nature, not deductible

- Interest accrued during vacancy — not deductible, no income being produced

Maintenance Fees, Sinking Fund & Utilities

Strata maintenance fees, sinking fund, and IWK

For strata properties — condominiums, service residences, SOHOs, and gated landed strata — the monthly maintenance fees and sinking fund contributions paid to your Joint Management Body (JMB) or Management Corporation (MC) are explicitly listed as allowable deductions by LHDN. These are treated as direct costs of maintaining the property in a rentable condition, clearly revenue rather than capital in nature.

Indah Water Konsortium (IWK) sewerage bills are also deductible on the same basis.

- Monthly maintenance fee to JMB or MC

- Sinking fund contributions (10% of maintenance fee, statutory under Strata Management Act)

- Indah Water (IWK) bills — explicitly listed as allowable by LHDN

- Assessment tax (Cukai Taksiran) paid to local authority

- Quit rent (Cukai Tanah) paid to state authority

- Fire insurance premiums on the rental property

Keep your JMB payment receipts or bank transaction records for the full assessment year. These are clean deductions with no ambiguity — claim them without hesitation.

Repairs vs Renovations: The Critical Distinction

This is the most nuanced area of rental tax deductibility — and the one most commonly misunderstood. The answer is not simply "renovation is not deductible." LHDN draws a precise line between repairs (revenue expenditure, deductible) and improvements (capital expenditure, not deductible). The distinction turns on whether the work restores the property to its existing condition, or enhances it beyond that.

Repairs — restoring what was already there

Work that brings a deteriorated item back to its original functional condition — like-for-like, without enhancement — qualifies as a repair and is deductible as a revenue expense.

- Replacing a broken water heater with an equivalent model

- Repainting walls (maintenance repainting to original condition)

- Fixing leaking pipes or plumbing

- Replacing worn flooring with the same material and grade

- Replacing a faulty air-conditioning unit with a like-for-like model

- Fixing a damaged ceiling or wall caused by water seepage

Improvements — enhancing beyond original condition

Work that adds value, upgrades, or creates something that did not previously exist is classified as capital expenditure. LHDN specifically calls out expenses incurred to command higher rental or improve the property's appeal as capital in nature — disallowed under Section 4(d) even if the goal is ultimately to produce more rental income.

- Kitchen upgrades or full kitchen fit-out

- Adding built-in wardrobes that did not previously exist

- Installing air-conditioning where none previously existed

- Converting an open-plan area into an enclosed room

- New flooring installed over an existing surface (upgrade, not replacement)

- Any renovation to attract higher rent or make the unit more competitive

- Full interior design and furnishing packages

The Borderline Cases

Some expenses sit in genuinely ambiguous territory. Replacing all the flooring after a tenant caused extensive damage — is that a repair (restoring to original) or an improvement (new material, better finish)? In practice, LHDN assesses based on the facts and documentation. The burden of proof is on the landlord. If you are dealing with a large, ambiguous expense, document your reasoning: photograph the pre-existing condition, get contractor quotes that describe the work as restoration rather than upgrade, and if the amount is material, consider seeking a professional tax agent's opinion before filing.

The Vacancy Rule

This is the condition that catches the most landlords off guard, particularly for new purchases or properties undergoing renovation between tenancies.

LHDN requires that deductible expenses be directly tied to the production of rental income. Without an active tenancy generating income, there is no qualifying income against which to offset any expenses — including mortgage interest, maintenance fees, assessment tax, or insurance. Expenses incurred during vacant periods, pre-tenancy renovation periods, or while the property is being prepared for rental simply do not qualify.

This has a practical implication for yield calculations: the true after-tax cost of a property purchase includes the months between handover and first tenancy during which carrying costs accumulate with no deduction offset. For new launches, this can span 3–6 months after vacant possession while the unit is renovated and let. Budget this period explicitly.

Non-Resident Landlords: The 30% Flat Rate

The deductibility rules above apply equally to resident and non-resident landlords — both can claim the same allowable expenses. The difference lies in the tax rate applied to the net chargeable income that remains after deductions.

| Residency Status | Tax Rate on Net Rental Income | Personal Tax Reliefs |

|---|---|---|

| Malaysian tax resident (≥182 days in Malaysia per year) | Progressive 0% – 30% | Claimable |

| Non-resident (<182 days in Malaysia per year) | Flat 30% on net chargeable income | Not available |

For a non-resident landlord, the effective deduction impact is straightforward: every RM 1 of allowable expense reduces your tax bill by RM 0.30. On a RM 1.5M property with RM 90,000 in annual rental income, a typical set of allowable deductions — loan interest, maintenance fees, assessment tax, insurance, and repairs — might reduce net chargeable income to RM 55,000. At 30% flat, that is RM 16,500 in tax versus RM 27,000 on the gross figure. The deductions are worth RM 10,500 annually — not trivial.

Quick Reference Summary

| Expense Item | Deductible? | Key Condition / Notes |

|---|---|---|

| Bank loan interest | ✓ Yes | Interest component only; property must be tenanted |

| Loan principal repayment | ✗ No | Capital repayment — not deductible under Section 4(d) |

| Maintenance fee & sinking fund | ✓ Yes | Explicitly allowable for strata properties; applies while tenanted |

| Indah Water (IWK) bills | ✓ Yes | Explicitly listed as allowable by LHDN |

| Assessment tax (Cukai Taksiran) | ✓ Yes | Allowable as a cost of holding rental property |

| Quit rent (Cukai Tanah) | ✓ Yes | Annual land tax; deductible |

| Fire & home insurance | ✓ Yes | Premiums on the rental property are deductible |

| Repairs (like-for-like restoration) | ✓ Yes | Must restore existing condition — not enhance or upgrade |

| Renovation & improvements | ✗ No | Capital expenditure — not allowable, including work done to attract higher rent |

| Property management fees | ✓ Yes | Fees paid to a licensed property manager are deductible as a cost of producing income |

| Expenses during vacancy | ✗ No | No income being produced — no deduction applies, including loan interest during vacant periods |

| Personal reliefs (non-resident) | ✗ No | Available to residents only. Non-residents pay flat 30% with no personal reliefs |